Personal Tax for Small Business Owners

An overwhelming amount of scattered guidance exists for business owners filing their taxes. Here is a consolidated record of need-to-know info for self-employers.

With or Without an Accountant

Whether you file yourself or have an accountant, it is critical to understand the basics of the tax process if you own a small business or are self-employed. Accountants are expensive and while some charge per filing, others charge by the hour. Even those who charge per filing will often bill extra if you come to them at tax time with disorganized records. Approaching the process with basic knowledge of what you will need and organized, accurate documents will keep money in your pocket.

Depending on how complicated your tax situation is and how well you understand the process, it is possible to file yourself, avoiding the fees accountants charge. Either way, knowing the tax implications of financial decisions throughout the year will help you navigate ways to save. For more background and information on organizational taxes please refer to my previous article: ‘Preparing to File Your Taxes’.

That's the Wind-Up; Here’s the Pitch

Let’s discuss a few scenarios that might apply if you operate a single-member LLC, a nonprofit, and/or are self-employed.

If you have an incorporated organization - an LLC or 501(c)(3), for example - and take a regular salary, you classify as a W-2 employee. If the organization is for profit, any additional income from profits will be taxed as an “owners draw”. You will not receive a 1099 for this income - it will be “passed through” to you and be reported on your individual return (Schedule C). It will be taxed as self-employed earnings. If you do not take a salary from your LLC, all of the earnings will be taxed this way.

If you have a nonprofit, the organization must file Form 990. If you take compensation as a contractor rather than salaried employee, the organization must issue you a Form 1099 showing the compensation you received. You will then report that income on Schedule C of your individual return.

If you do not have an incorporated entity but have business-related income, you will receive 1099(s) (usually type NEC, non-employee compensation) from the businesses that paid you to report on Schedule C. Note, however, that if you received less than $600 from any particular organization in that year they are not required to issue you a 1099, but you still must report the income on Schedule C.

Finally, If you are an LLC owner and elect to file as an S-Corp., or a partner in a multi-member LLC (partnership), there are different tax implications and reporting requirements that I will address in a future article.

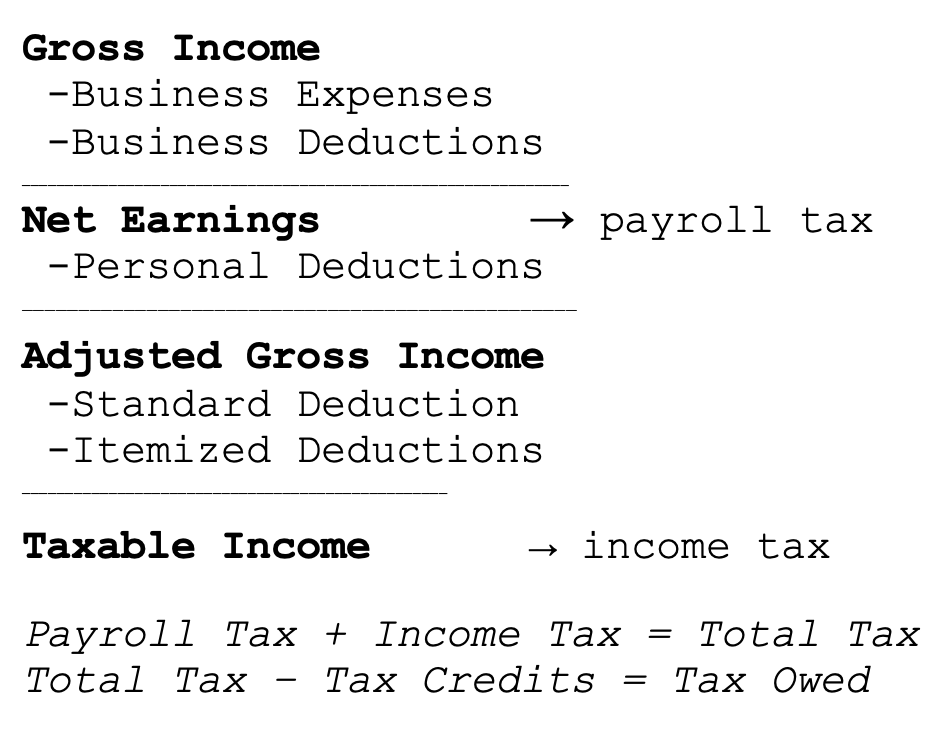

Federal tax for individuals has two components: payroll tax and income tax. Below is what I call a Personal Tax Profit and Loss Statement - a P&L that is clear and simple, and, for some reason, doesn’t exist on the IRS website or anywhere else on the internet.

Payroll Tax plus Income Tax is Total Tax. Any Tax Credits you qualify for will reduce the amount owed dollar-for-dollar. Common credits include Earned Income Tax Credit (EITC) for lower incomes and Child Tax Credit (CTC) for parents and guardians. Total Tax less Tax Credits is the amount of tax you owe.

Gross Income is the total amount of business-related income you had from sales through an LLC or compensation as a contractor.

Business Expenses are money spent in the course of business operations for things like supplies, marketing, rent, and personnel.

Business Deductions are non-cash costs to operating business. Common examples include vehicle mileage, home office use, portions of communications utilities (cell phone, internet), and self-employment deduction.

Net Earnings are Gross Income less Business Expenses and Deductions. This is the amount payroll taxes apply to. For self-employed earnings the rate is 15.3%, for W-2 employees it's 7.65% - the employer pays the other half.

Personal Deductions are certain costs incurred not related to business such as health insurance premiums, student loan interest, and retirement contributions.

Adjusted Gross Income (AGI) is Net Earnings less Personal Deductions. The IRS does not tax based on AGI but it uses this figure to limit certain deductions and credits and determine eligibility for some tax programs, such as credits for Marketplace health insurance.

Standard Deduction is a fixed amount the IRS allows everyone to exclude from their taxable income. For individual filers the 2025 amount is $15,750 (twice that for taxpayers filing jointly). You can elect to use this deduction or itemize other deductions and choose whichever amount is greater to reduce taxable income.

Itemized Deductions are other qualifying personal costs such as state and local taxes (SALT), mortgage interest, medical expenses >7.5% AGI, and charitable contributions. If the total of these is less than than the standard deduction there is no need to itemize them.

Taxable Income is AGI less the Standard Deduction or Itemized Deductions. This is the amount income tax is based on. I will provide a brief explanation of tax brackets below.

Other Nice-to-Know Items

Unlike payroll taxes, income tax is not a fixed rate across all income. Taxable income is taxed in brackets with lesser amounts taxed at lower rates. Using rounded numbers, here are the current federal income tax brackets:

$0-12,000 (10%) - $1,200 if above

$12-49,000 (12%) - $4,440 if above

$49-103,000 (22%) - $11,880 if above

$103-197,000 (24%) - $22,560 if above

*brackets continue up to 37% of income over $626,000

Marginal tax rate is the rate of the highest bracket you have income in. Effective tax rate is the amount of income tax you owe divided by taxable income. If you have $70,000 of taxable income you pay a 22% marginal rate on income from $49-70,000 and have $10,260 of total income tax liability, a 14.7% effective rate.

To 1099 or W-2, That is the Question

1099 employment and forms are for individuals who provide one-time or limited scale support to an organization. W-2 employment is for individuals who are hired for an indefinite amount of time to support ongoing work. In some cases it is clear how an individual's compensation should be classified and there are penalties for misrepresenting a person’s work type. In other situations, a person’s work type may not be straightforward; choosing how to classify has significant implications for the organization and individual. Below is guidance directly from the IRS:

The general rule is that an individual is an independent contractor if the person for whom the services are performed has the right to control or direct only the result of the work and not what will be done and how it will be done.

Under common-law rules, anyone who performs services for you is your employee if you can control what will be done and how it will be done.

But in some cases this leaves room for interpretation. People who receive 1099s are self-employed by definition and should be referred to as ‘independent contractors’’, not ‘employees’. Those who receive W-2 forms are ‘employees’.

Independent contractors do not have taxes withheld from their compensation and they are responsible for paying all of their taxes including full payroll tax (15.3%). For W-2 employees, employers are required to withhold state and federal taxes from their compensation and also pay half of the payroll taxes (7.65% employer/7.65% employee). Payroll taxes, often referred to as FICA, are a combination of Social Security and Medicare taxes. Employees are often offered health insurance, paid time off, and/or retirement programs while contractors are generally not eligible to receive these benefits. Contractors have limited legal protections while employees are covered by federal and state unemployment regulations. Organizations may lean toward choosing 1099 employment for workers where possible; independent contractors are less expensive to hire.

If you run a small organization and determine you could qualify as either a contractor or employee there are pros and cons to either way you classify employment. If you are the business owner, whichever compensation type you choose you will owe full payroll tax on earnings (either all as a contractor or half as an employee, half as an employer). A key difference is that as a contractor you can deduct business expenses like vehicle use and home office costs from income to reduce Net Earnings and lower payroll taxes. Employees cannot deduct business expenses to lower earnings, all W-2 income is subject to payroll tax. However, organizations can offer reimbursements to employees for costs like vehicle use and utilities (internet, phone) so reclassifying some compensation as reimbursable expenses can effectively achieve a similar result (there are accounting requirements for reimbursements).

Additionally, as an employee, the organization can pay your health insurance premiums, shielding those amounts from payroll taxation (self-employed premiums are deducted after Net Earnings as personal deductions). There are other benefits for employees to W-2 employment such as unemployment and disability insurance, ease of getting personal loans (mortgages), and retirement planning. While W-2 employment is almost always an advantageous for the employee, remember that if you plan on effectively being both the employee and the employer that W-2 compensation comes with requirements like federal and state withholdings and quarterly filings. 1099 income has more flexibility and fewer requirements while W-2 income generally has more potential benefits. All things to consider if it is unclear how to classify your compensation if you run your own organization.